ESG Year-end 2022 Review

Pitfalls & Opportunities

ESG is the buzz-acronym of the decade, let alone 2022. There was a modest pull-back in the enthusiasm for ESG Integration, an additive consideration in the traditional investment process. This ESG construct is the “new normal”, not just the flavour of the day. Greenwashing will hopefully be policed with more precision going forward. Those investment firms that actually invest incorporating ESG metrics in their decision making will win out in the end.

Texas and Florida have been siphoning tri-state (CT, NJ, NY) taxpayers for years with great success. Ron DeSantis in Florida recently blocked state pension fund managers from incorporating ESG factors into their investment decisions. Texas moved to ban 10 managers from managing state pension assets on similar ground (most notably Blackrock, the largest investment manager globally with $11tln AUM).

ESG AUM (asset under management) is expected to grow to $34 trillion globally by 2026 ($18.4 tln as of 2021) Note: With a more “rigorous ESG definition applied, the 2021 ESG AUM is $8tln. ESG mutual funds and ETFs saw 53% growth in 2022 and stand at $2.7 trillion. For context, the total aum for the mutual fund industry globally is approx. $18 tln and ETFs now exceed $7 tln (ETF growth rate at least 2X mutual funds).

Returns year-to-date 2022 through Dec 26, 2022:

SPY - SPDR S&P Index, aum 372bln, -18%

QQQ - PowerShares NASDAQ-100 Index, aum 166bln -32%

SPYX - SPDR S&P Index Fossil Fuel Free ETF, aum 1.3bln, -20%

USO - United States Oil Fund ETF, aum 3bln, +28%

UNG - United States Natural Gas Fund, aum 0.5bln, +27%

DBO - PowerShares DB Oil Fund, aum 0.6bln, +11%

Largest ESG ETFs:

ESGU - iShares ESG MSCI USA ETF, aum 23bln, -20%

ESGV - Vanguard ESG USA ETF, aum 6bln, -24%

ICLN - iShares S&P Global Clean Energy ETF, aum 5.1bln, -5%

ESGD - iShares ESG Aware MSCI EAFE, aum 7.1bln, -15%

VSGX - Vanguard ESG International ETF, aum 3bln, - 19%

NUMG - Nuveen ESG Mid-Cap Growth ETF, aum 0.3bln, - 29%

ESG rating methodologies vary widely with divergent data inputs. The “E” component is the 1st and gets a perhaps an undue amount of the limelight, given concern over climate change and net-zero transition pathways. In reality, most ratings weight each component equally.

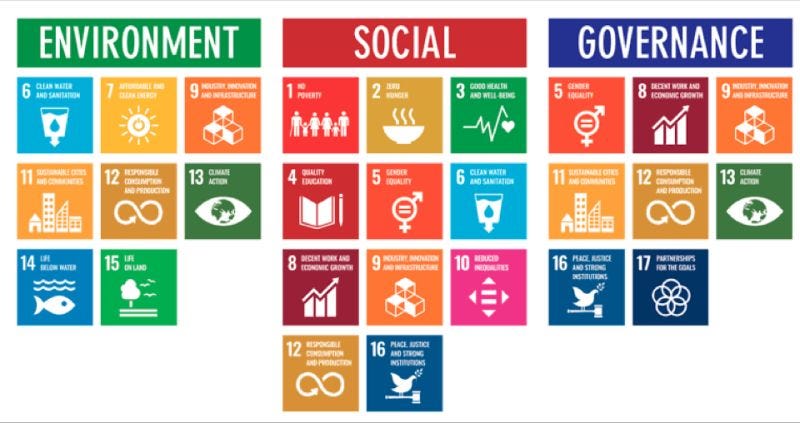

Aug 2020 ESG Recap (Background)

How ESG and the UN STG’s (Strategic Development Goals) align. Ballpark only! All are inter-related.

The global economy is certainly not “anti-fragile” with respect to climate disasters and their lingering financial impact. Extreme weather events are trending higher, it is not our imagination. The New York Times noted that the last 42 years there were 8 US climate events with damages/insured losses > US$1bln. From 2017 to 2021 this stood at 18 per annum. Insured losses for the USA now regularly exceed $100bln. The average for the last decade is $75bln per annum. The 5% aggregate exceedance probability (EP) for insured losses (20 year return period loss) is $203bln, source Verisk. The 1% EP (100 year return period loss) is $320bln.

In the US roughly 1/2 of weather related losses (hurricane, wildfires, flooding, all perils) are insured. As one might assume, the % insured in emerging markets is much lower.

The insurance and re-insurance industry has capacity limits. Regions and whole countries may become uninsurable, outright or for specific perils.

Going forward, enhanced due diligence is required to ferret out those companies, regions and sovereigns at elevated risk of destruction/damage to physical assets and critical infrastructure from hurricanes, floods and fires.

Pakistan floods in 2022 resulted in economic damages of $30bln, not to mention the 1,700+ loss of life and millions negatively effected. Little of this loss was insured. COP (Conference of the Parties) 27 in Egypt this year tabled the concept of “Climate Reparations”, with some experts estimating that, if such a mechanism existed, the wealthy developed nations of planet Earth would be deemed 50% responsible, hence a $15bln funding requirement. With global debt at $88 tln (equal to, 100% of global GDP of $88tln) it is difficult to see this concept being embraced. US national debt stands at $31.5tln or 35% of the total.

Investing in financial institutions will require an ESG view/filter as well, given that they lend to and in some cases insure downstream players in the global economy. Global bank regulators (Basel) have proposed a higher capital charge against assets that support the fossil fuel industry.

Renewable energy can not pull the sled on its own. Traditional power generation will incorporate fossil fuels for the foreseeable future (well beyond the 2050 net-zero timeframe). The goal should be to have natural gas displace coal. Nuclear, including 2022 advancements in nuclear fusion has to be part of the global solution. Carbon dioxide makes up 75% of total emissions. There is presently 410 ppm of carbon dioxide in Earth’s atmosphere. The current 34bln tonnes per day of CO2 must track to 15bln/day (<60%) by 2040 to meet net-zero 2050 commitments and Paris Accord commitments to limit global temperature rise to +1.5-2.0 degrees (Paris was COP21 held in 2015).

Green commodities. The World Bank estimates that 3bln tonnes of metal and minerals for renewable energy infrastructure will be required by 2050, heavily weighted towards the coming decade. Lithium and cobalt, 6x present use, copper (25+kg in each EV battery) 2x, nickel 4x, aluminum - more, silver -more cowbell. Uranium to the moon (ATH, all time highs)!

Do morals and money mix? To my mind, as both a CFA and FRM charter holder, ESG is a risk management tool. ESG is potentially a factor (equal-weighted components) that has explanatory power about the potential risk-adjusted returns of an asset. Could a 2-factor model CAPM (Capital Asset Pricing Model), using Markowitz’s 1-factor Beta (beloved for its simplicity of application) and ESG (as an additive additional factor) outperform the 3-factor Fama-French model over the coming decade? I would resoundingly vote yes.

Impact investing is a different ESG sub-species where ESG is a an outcome, something to be achieved, a destination (Eden). Broader stakeholder accountability likely means < shareholder returns in the short run, but may be the best strategy for the ultra long term (this sounds a lot like Japan, as an aside).

ESG is tough sledding when nominal return in risk assets (equities) and bonds (typically seen as a hedge) are double digit negative ytd in 2022. The S&P is down 18.1% ytd, the first decline since 2018 and the worst performance since the 2008 GFC. Bonds are having their worst outing since 1940. When oil & gas is one of the few sectors up, it is natural for investors to feel hoodwinked. Davos, WEF, FTX, etc. make folks thing the only wool that exists is that pulled over their droopy eyes. It will take time and execution to build trust.

Non-correlated assets. Hard to come by, in size. The tradable carbon market is growing ($700bln in 2021). Positive risk adj. returns and relatively uncorrelated with other asset classes. High vol, hence not for the meek (lower annualized vol than crypto, but too much risk for many).

More countries will adopt a carbon pricing plan going forward. Canada’s carbon pricing initiative was centre stage at COP27 this year in Egypt. C$50/tonne in 2022 stepping up $15/tonne per year (C$65/tonne from Jan 2023) until reaching C$170/tonne in 2030. Climate Action Incentive Payments (love the naming nomenclature) are expected to avg. $248 per quarter in Nova Scotia with “most” residential customers receiving 10% more in incentive payments than they pay in carbon tax. Brings to mind the adage, “I am from the government and I am here to help.”

Canada is a huge country. Converting from oil to renewable is a big $ ticket and the fragile grid means a substantial investment in “off-grid” solutions when the grid is down for myriad reasons (ice, heavy snow, trees down, quick fixes for prior outages):

3,000 sq. ft home example:

Oil/hot water to Heat pump conversion C$10,000 (payback 4.5yrs)

Solar array 12 kW, $29,000 ($23k net of subsidy, payback 8.5yrs)

Back-up battery storage $18,000 = $51,000 net total cost (approx. 7 year payback).

Summary:

This will not be easy. This must be done. We can do this. Happy New Year to all. JCG