Best-efforts

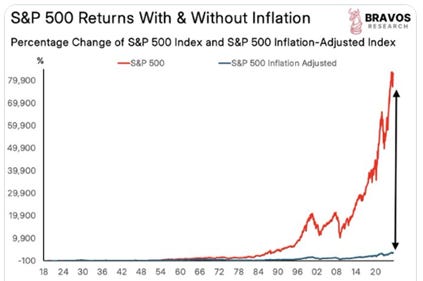

What havoc inflation wreaks; bonds, equities, precious metals and pensions plans

Best-efforts (Merriam-Webster)

adjective

best-ef·forts

of security underwriting

: not involving a firm commitment on the part of an underwriter to take up any unsold shares or bonds of an issue being underwritten

Capital Markets:

The term “best efforts” was coined in 1969. It can be contrasted with a “bought deal” in the Canadian market, a firm-commitment underwriting where the underwriter (or syndicate) agrees to purchase the whole issue, often before marketing. Typically used for secondary issues by publicly traded firms. Characterized by quicker execution, and sends a strong signal of confidence. Typically priced at a discount (to compensate the underwriter for the market/execution risk assumed).

Pensions:

We have seen “best efforts” used in the defined benefit pension as well. OMERS (Ontario Municipal Employees Retirement Savings Plan) is a notable pension plan in Canada, with $138bln in AUM (vs. $778bln for federal CPP, $473bln for Quebec’s CDPQ, $112bl for Ontario’s HOOPP and $180bln for Albert’a AIMCo.

Annual inflation increases (cost of living increases) are linked to CPI.

OMERS adjusts pensions each January based on the change in the Canadian Consumer Price Index (CPI) over a 12-month period ending in October. This is similar to how the Canada Pension Plan does it.

Two parts of one’s OMERS pension are now treated differently:

Benefits earned before January 1, 2023, receive full inflation protection, i.e., 100 % of the CPI increase, up to a maximum of 6 % per year. If inflation exceeds 6 %, the excess can be carried forward to a future year when inflation is lower.

Benefits earned on or after January 1, 2023, are subject to Shared Risk Indexing (SRI). Under SRI, inflation increases are not automatically guaranteed, the OMERS Sponsors Corporation Board evaluates the financial health of the plan yearly and decides how much inflation adjustment to grant, up to 100 % of CPI.

This conditional part is why people sometimes describe the current approach as a “best effort” or conditional inflation plan: the board aims to match inflation but doesn’t absolutely guarantee 100 % CPI indexing on post-2022 service unless the plan’s funding situation supports it. For 2025 the increase was 2.61 % and for 2026 it’s 2.00 %. In those years, full CPI indexing was granted despite the SRI framework, given that the inflation increases with modest/benign and did not imperil the health of the plan.

Most private pension plans offer no indexing (i.e. inflation protection) and some government plans only offer partial (Alberta government pension offers 50% of CPI).

USA direct federal debt stands at US$38.5tln and is slated to hit $40tln in 1H 2026. Within 4 years 73% of this debt will mature and need to be refinanced. Total interest expense of approximately $1tln now eclipses the USA Department of War budget. Total unfunded obligations of the US government have crested $100tln and 75% of these government IOU’s are inflation protected (in favour of the recipients, potentially increasing the size of the liability significantly over time).

The total bond market is $300tln presently, 3x global GDP of $100tln. The pain does not spread even when it comes to servicing this debt. Emerging markets end up in a dead pool default lottery and countries like Japan with the highest debt/GDP in the G10 suffocate as bond yields take out multi-decade highs. The BoJ hiked rates by 25bp last week to 75bp, the highest in 30 years. Japan’s QE (quantitative easing) program is of the “kitchen sink” variety and includes all asset classes, including equities.

Pareto Principle. 80% of wealth is controlled by 20% of the population. This has been a long standing truth is democracies for as long as economics have been studied. Income/wealth inequality have become more severe, if anything, with the top 1% garnering 50% of the “spoils”. Global central bank policy and AI have set us up for a record wealth gap.

From a pension perspective, most individuals are relegated to defined contribution pension plans with a “match” from their employer. The risk is the employees with respect to performance (the 7% “steady” annual performance masked & pitted by 3 market crashes in 25 years, so called 100 year events by the statisticians) and, as noted, most do not offer any form of protection/back-stop with respect to inflation.

Financial literacy remains low overall with undue complexity hoisted upon a largely unsuspecting populace. Most do not know where to turn and feel the affordability pinch in their monthly budget. When does the pressure subside to allow for prudent planning for our extended families? Life and disability insurance. Retirement planning. Education saving plans. Medical insurance. The list can seem endless.

Credit card debt in the US has crested $1.3 tln (US$8,125 avg. balance). The majority of card holders are now struggling with their credit card debt. 40% of those making >100k per year are behind on their BNPL (but now pay later) instalment payments. Klarna, PayPal’s BNPL platform and Affirm will undoubtedly bring more harm than good to the masses.

AI:

Having spent a few inning in academia (finance, risk management, investments, insurance) I would like to think the glass is 1/2 full, but the current “free” offerings that are used by the early adopters reeks and ultimately produces slop, without a real world, human edit.

In an effort to up my personal AI “game” I am currently enrolled in the Risk & AI Certificate course offered by the Global Association of Risk Professionals (GARP) and will be sitting for the 4 hour exam in early April 2026. Tough content, but continuing ed is not all fun!

Note: Sam Altman, CEO, Open AI. Provided without comment.

Quote(s):

“I look back on it now, and it all seems so trivial…I spent my life in the toy department of human existence.”

~ Howard Cosell, death bed regret

“Governments like the United States are unwilling or unable to constrain the power of the capital classes, and humanoid automation will only strengthen their hand. The future that scares me in not a robot uprising led by the robots, but one led by billionaires. And that is the direction we’re currently headed in.

~ James Vincent

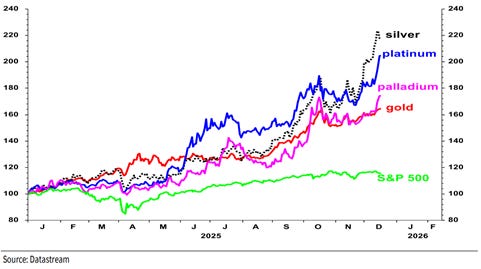

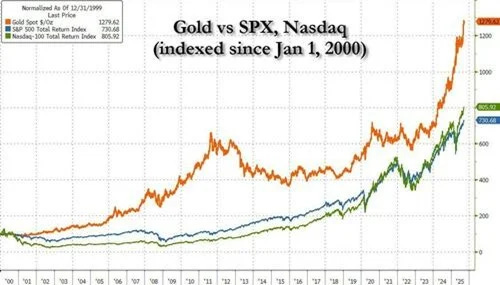

Precious metals:

Silver, gold and platinum have investors/traders full attention as we finish out 2025. Silver is up > 140% ytd and has crested US$76 oz. in Asian trade. There is a global supply shortage and the physical market can not longer satiate soaring demand. The 300:1 ratio of paper($SLV et al) to physical silver is proving “challenging”. JP Morgan at $4tln + in assets is almost 20% of the entire US banking system. To big to fail …. indeed. JPM, known via convictions and fines for same are know to Amy Winehouse the precious metals markets with some frequency. They recently flipped a 250 million ounce short position into a 750 million ounce long which may be proving a “thumb on the scale” which coincides with new China export rules slated for the new year (the year of the “Fire Horse” in the Chinese zodiac. Short at your peril!

Crypto:

Crypto has been “risk off” in Q4 2025, -30% at $87,450, down from recent highs of US$125,400 in Oct 2025, erasing much of the tRump exuberance since the beginning of his 2nd term. Rumours are of some degree of reallocation from crypto to precious metals in the last month. 40% of money managers have 0-1% allocated to precious metals and those with 10% allocated will likely stay on the gas before reallocating. They say if you can find a bubble, buy it. Silver >, BTC <. The AI advances and investment acting as the jazz hands to take risk assets higher could be the death knell for crypto if the non-zero eventuality that the blockchain is broken by the power of same. Digital gold …. indeed.

Equities:

Equity markets are not the economy. The outsized investment in AI related infrastructure appears excessive (data centres, extending the operating life of nuclear plants, etc.). The latest and greatest LLM’s (large language models) are currently depreciated over a comparable time frame to servers (5 years). Increased capex and lower margins for me puts this in the “Hopeism” camp until proven otherwise. Oracle’s outsized investment swing is partially debt financed, which to my mind is worrisome. Some peg the froth at 17x the dot.com bubble and some of us know how that ended. The federal reserve last cut Fed Funds by 25bp with 3 dissenting vote (most since 1988). tRump is hell bent on politicizing the Fed Chair role. Many expect just 1 more hawkish ease in 2026. The tepid pace of quantitative tightening was ceased, juicing M2 going forward.

Private equity:

Fees in the PE space are 7-10%, resulting in most research stating that the “alpha” over public equity markets is close to zero, once you factor in the lack of a proper mark-to-market (mtm). Large endowments like Harvard ($53bln) have allocations as high as 40% to “alts” which include PE. The lack of liquidity and resultant disruption caused to liquidate has led Harvard and others to issue debt to fund their more immediate cashflow needs. Hopeism might not be a strong enough phrase here … perhaps “running with scissors”.

Book recommendations:

“The Richest Man in Babylon” 1926 George Samuel Clason

“The Price of Time, The Real Story of Interest” 2022 Edward Chancellor

Best wishes for 2026. Hoping you enter the new year well rested and up for the challenges that lie ahead.

Cheers,

JCG